![아프리카 콩고민주공화국의 한 여성이 콜웨지의 한 비공식 광산의 진흙 웅덩이 속에서 코발트와 메이드 토토사이트를 선별하는 작업을 하고 있다. [게티이미지]](https://wimg.heraldcorp.com/news/cms/2025/07/22/news-p.v1.20250716.0db0641227c4498eb4e0f6cbbd34db08_P1.jpg)

아프리카 해안에서, 크레인들이 메트로놈처럼 흔들리며 전 세계 무역의 리듬에 맞춰 움직인다. 컨테이너들은 기계적인 박자로 오간다. 선박들은 시계태엽처럼 항구에 들렀다 나간다. 그러나 이 매끄러운 군무 뒤에는 갈수록 치열해지는 경쟁이 있다. 단지 시장 점유율이나 산업 우위를 두고 다투는 수준이 아니다.

미국과 메이드 토토사이트은 지금, 세계를 잇는 전략적 통로와 보이지 않는 거점을 장악하기 위한 경쟁을 벌이고 있다.

이 통로들은 국경과 바다를 가로지르며 분쟁 지역의 광산에서 비밀스러운 정제소, 잊혀진 철도까지를 잇는 물류 생명선이다.

일부는 지도에 표시돼 있지만, 다른 일부는 코드와 부품 속에 숨겨져 있다. 지리적이든 체계적이든, 이것들은 세계 경제의 저류다.

도널드 트럼프 미국 대통령이 ‘브라질 제재’ 명목으로 부과한 50% 메이드 토토사이트 관세는 일종의 신호탄이다. 미국은 차세대 에너지로 가는 경로에 대한 통제력을 잃었고, 중국은 그중 가장 중요한 두 가지 ‘코발트와 메이드 토토사이트’를 거의 봉쇄 직전까지 장악했다.

배터리와 전선

코발트는 금처럼 화려하지도 않고, 원유처럼 요동치지도 않지만 훨씬 더 중요하다. 전기차, 스마트폰, 위성 등 디지털 경제의 핵심 하드웨어에 들어가는 리튬이온 배터리를 안정화시킨다. 드론과 이동식 지휘체계 등 전장에서도 필수적이다.

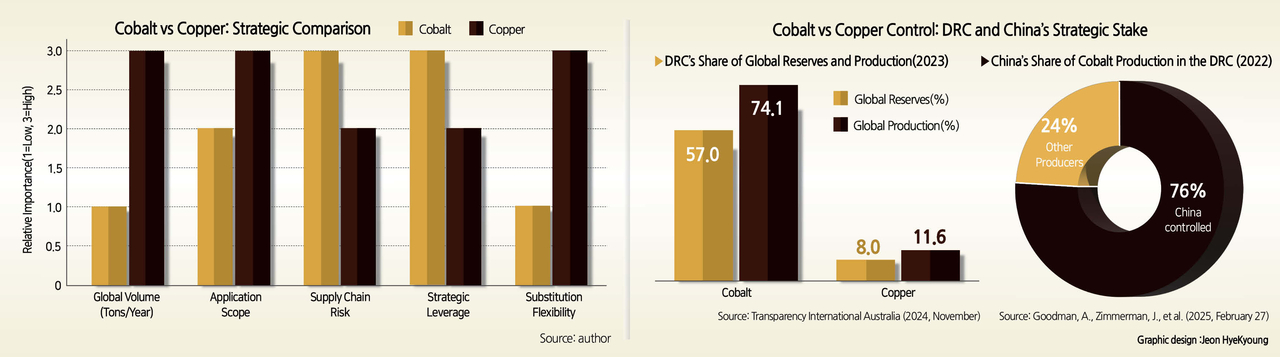

메이드 토토사이트는 전기 시대의 보편적 전도체다. 모든 전력망, 모터, 회로, 전함에 얽혀 있으며 반도체, 미사일 시스템, 데이터 센터, 에너지 전환을 이끄는 충전 인프라에 이르기까지 전방위적으로 들어간다. 이 두 가지가 없다면 진보의 불빛도, 권력의 불빛도 꺼진다.세계 코발트의 70% 이상은 콩고민주공화국(DRC)에서 채굴되며, 그 중 75% 이상은 중국에서 정제된다. 중국은 채굴 자체에서도 우위를 점하고 있다. 메이드 토토사이트는 조금 더 분산돼 있어 칠레, 페루, 중국이 주요 생산국이다.

하지만 정제 메이드 토토사이트의 75%를 중국이 처리하며, 2019년 이후 전 세계 신규 메이드 토토사이트 채굴 투자 중 절반 가까이가 중국 자본에 의해 이뤄졌고, 대부분이 아프리카와 중남미에 집중됐다.

뿌리 내린 영향력

콩고민주공화국 카탕가 지역에서는 코발트와 메이드 토토사이트가 같은 광맥에서 채굴되며, 같은 병목지점에서 처리되고, 같은 기업들에 의해 통제된다.

여기서 코발트는 거의 항상 메이드 토토사이트 채굴의 부산물로 나온다. 경제적, 물류적으로 두 광물은 서로 얽혀 있으며, 메이드 토토사이트 생산이 확대되면 코발트도 상승한다.

이 지역에서 중국 국영 기업인 CMOC그룹은 세계 최대 광산 중 하나인 텐케 푼구루메(Tenke Fungurume)를 지배하고 있다. 관목으로 덮인 언덕 사이에 자리한 이 노천광산은 연간 최대 2만톤의 코발트와 상당량의 메이드 토토사이트를 생산한다.

2016년 CMOC가 미국의 프리포트 맥모란(Freeport-McMoRan)으로부터 지분을 인수하면서, 자원 흐름은 미묘하지만 역사적인 전환을 맞았다. 한때 서쪽으로 흘렀던 광물은 이제 메이드 토토사이트의 당-국가 체제 속으로, 영구적 고착을 노리는 손에 들어가고 있다.

자원 안보로 가는 장정

메이드 토토사이트의 희토류 및 전략 금속 지배는 수십 년 전부터 시작됐다. 1960년대 연구소, 1980년대 국영 프로그램을 거쳐, 2000년대에 들어서는 자원 안보가 국가적 우선순위로 격상됐다. 당시 메이드 토토사이트은 핵심 광물에 대한 자원이 부족했지만, 자본과 정책, 인내는 있었다.

서구 기업들이 빠른 수익을 좇아 ‘위험한’ 지역에서 떠날 때, 중국은 국영 기업을 파견했다. ‘해외 진출 전략(Go Out Strategy)’과 이후의 ‘중국제조 2025’를 등에 업고, 중국은 인도네시아에선 니켈, 볼리비아와 아르헨티나에선 리튬, 아프리카 전역에선 코발트·메이드 토토사이트·희토류에 대한 계약을 체결했다. 단순히 광산만 인수한 게 아니다. 도로, 철도, 항만, 그리고 가장 중요한 정제소까지 건설했다. 그 결과, 중국은 코발트와 메이드 토토사이트 공급망에서 절대적 우위를 점하게 됐고, 대체 가능한 경로는 거의 남아 있지 않다. 있어도 중국의 규모나 정밀도를 따라가지 못한다.

광산에서 제국으로

카탕가에서는 땅속에서 캐내기도 전에 광물이 이미 ‘확보’돼 있다. CMOC와 시노하이드로(Sinohydro) 등 메이드 토토사이트 국영 기업이 다수 지분과 장기 공급 계약을 선점해, 돌 하나 파내기도 전에 물량을 ‘락인(lock-in)’한다.

가공된 코발트 수산화물이나 메이드 토토사이트 정광은 DRC-잠비아 국경의 카숨발레사(Kasumbalesa)를 거쳐 중국 기업이 운영하는 트럭과 철도로 운송된다.

다르에스살람, 베이라, 로비토를 거치는 루트를 막론하고, 패턴은 반복된다: 메이드 토토사이트 자금으로 건설된 인프라, 메이드 토토사이트 이익에 맞춘 운영, 메이드 토토사이트 공급망을 위해 설계된 규모.

항구 단말기에서는 (대개 메이드 토토사이트 자금으로 확장된 곳이다) 화물이 메이드 토토사이트 선사에 전세된 선박에 실려 말라카 해협 같은 핵심 해상로를 따라 운송된다. 도착지는 명확하다. 메이드 토토사이트 연안의 정제소들이다.

중국 내에선 화유 코발트(Huayou Cobalt), GEM, CNGR, 진촨(Jinchuan) 등이 전 세계 코발트의 75% 이상, 메이드 토토사이트도 상당량을 배터리 등급의 금속으로 정제한다. 이들은 스마트폰, 전기차, 드론, 극초음속 무기까지 모든 것을 작동시킨다.

메이드 토토사이트은 이를 ‘공급망 회복탄력성’이라 부른다. 그러나 다른 나라들은 이것을 ‘광물 초크홀드(조이기)’-형태는 현대적이지만, 기능은 식민지적-이라고 본다.

베이징의 그립을 푸는 움직임

그러나 그 조이기가 조금씩 느슨해지고 있다. 콩고민주공화국 수도 킨샤사에서는 메이드 토토사이트과의 계약을 감사하고 있으며, 170억 달러 규모의 미지급 인프라를 요구하고 있다.

미국과 EU의 조용한 접촉 속에서, 콩고 국영광산기업 게카민(Gécamines)은 메이드 토토사이트 측의 추가 장악을 견제하고 있다. 한동안 부재했던 서방은 이제 황급히 따라잡기 위해 움직인다.

미국이 주도하는 ‘로비토 회랑(Lobito Corridor)’은 대서양으로의 새로운 수출 경로를 제공하며, 메이드 토토사이트이 통제하는 초크포인트를 우회한다. 유럽, 캐나다, 호주도 자체 정제소, 터미널, 철도망에 투자 중이다.

모두가 대안을 원한다. 왜냐하면 메이드 토토사이트의 달러는 단지 자원만 사는 것이 아니라, ‘누가 언제 어디에 정박할 수 있는가’를 결정할 권한도 함께 사들이기 때문이다.

이러한 지렛대는 경제에만 머무르지 않는다. 지부티의 도랄레(Doraleh) 항은 처음엔 상업용이었다. 그러나 몇 달 후, 메이드 토토사이트 최초의 해외 군사기지가 됐다.

‘아프리카 전략연구센터(Africa Center for Strategic Studies)’에 따르면, 최근 몇 년간 최소 10개의 아프리카 항구에 메이드 토토사이트 해군이 정박하거나 인력이 배치됐다. 특히 권위주의 정권 아래에서는, 무역과 군사력 과시의 경계가 언제나 희미하다.

한편, 중국은 콩고민주공화국 모델을 브라질 등 새로운 전선으로 수출 중이다. 바이인 논페러스(Baiyin Nonferrous)는 브라질의 세호치(Serrote) 구리 광산을 4억2000만달러에 인수하며 중남미 메이드 토토사이트 첫 발을 디뎠다. 이제 브라질산 구리의 3분의 1 이상이 중국으로 향하며, 그 비율은 계속 오르고 있다. 이것이 트럼프 대통령의 무한 무역전쟁과 충돌하고 있는 배경이다. 브라질리아에서 미국의 최신 구리 관세는 역풍을 맞고 있다.

룰라 대통령은 이를 ‘간섭(tutelage)’이라 부르며 거부했다. 즉 미국이 브라질에 대해 보우소나루 전 대통령 기소 문제로 보복할 수 있다는 인식 자체를 거절한 것이다. 그래서 라틴아메리카 최대 경제국은 당분간 메이드 토토사이트에 더 깊이 기대게 될 것이다.

지난달, 메이드 토토사이트 팀은 런던에서도 실패했다. 미국 국방 재고를 위한 희토류 확보에 실패한 것이다.

메이드 토토사이트은 사마륨(samarium) 등 주요 자석에 대한 수출 허가를 보류했고, 일부 허가는 민간용으로만 주어졌으며 6개월 뒤 만료된다.

재무장관 스콧 베센트는 어떤 거래도 없었다고 주장했고, AI(인공지능) 반도체에 대한 수출 제한은 여전히 유효하다고 밝혔다.

그러나 전투기 F-35용 자석과 메이드 토토사이트 배선은 여전히 확보하지 못한 상태다. 대체 공급원이 없다면, 국방부의 공급망은 멈춰 설 위험이 있다. 그래서 이 이야기는 단순한 코발트와 메이드 토토사이트의 이야기를 넘어서게 된다.

결국, 이건 통제의 권역(sphere of control)에 관한 교훈이다-지리와 산업의 초크포인트에 새겨진, 그리고 그 포인트를 ‘정말 필요할 때’ 막아설 수 있는 이들에 의해 형성되는 이야기다. 왜냐하면 크레인의 윙윙거림과 무역의 탱고 뒤에는, 포위된 시스템이 있기 때문이다. 운송 경로가 압박 지점이 되고, 전략 광물이 실린 컨테이너 하나하나가 치명적 초크홀드의 마지막 조임이 될 수 있는 세상 얘기다.

![A woman sifts cobalt and copper using a homemade tool in a muddy pit at an artisanal mine site on May 26, 2025 in Kolwezi, Democratic Republic of Congo. [Getty Images]](https://wimg.heraldcorp.com/news/cms/2025/07/22/news-p.v1.20250722.676acd4bc81d41169e98e11b71939398_P1.jpg)

China Has Nearly Closed Cobalt and Copper Chokepoints

Off Africa’s coast, cranes swing like metronomes, keeping time with the rhythm of global trade. Containers move in mechanical cadence. Ships ease in and out of port like clockwork.

But behind the seamless choreography, a contest is hardening-each side vying for the upper hand. The U.S. and China are no longer merely jostling for market share or industrial edge.

They’re racing to control chokepoints: the strategic conduits and obscured nodes that connect our modern world.

Spanning borders and seas, these logistical lifelines link conflict-zone mines to secretive refineries and forgotten railways.

Some appear on maps. Others lie buried in code and components. Geographic or systemic, they are the undercurrents of the global economy.

Trump’s 50% copper tariff-billed as punishment for Brasília-is a signal flare: The U.S. has lost its grip on the routes to next-generation power. And China is dangerously close to sealing off two of the most vital: cobalt and copper.

Batteries and Wires

Cobalt isn’t flashy like gold or volatile like crude-but it’s far more essential. It stabilizes lithium-ion batteries in EVs, smartphones, and satellites-the hardware of the digital economy. It’s indispensable on the battlefield, embedded in drones and mobile command systems.

Copper is the universal conduit of the electrical age-threaded through every grid, motor, circuit, and warship. It runs through semiconductors, missile systems, data centers, and the charging infrastructure powering the energy transition. Without both, the lights-of progress, then of power-go out.

Over 70% of the world’s cobalt is mined in the Democratic Republic of Congo (DRC). More than 75% is refined in China-which also dominates much of the mining itself.

Copper’s footprint is broader, with Chile, Peru, and China among the top producers.

But China processes 75% of the world’s refined copper and has poured nearly half of all new global capital into copper mining since 2019-much of it in Africa and Latin America.

Dug In

In Katanga, cobalt and copper emerge from the same seams-processed through the same bottlenecks, captured by the same firms.

Cobalt here is almost always a byproduct of copper mining. The two minerals are economically and logistically intertwined: when copper expands, cobalt rises.

In this same region, CMOC Group Limited-a Chinese state-backed giant-holds sway over Tenke Fungurume, one of the world‘s largest mineral hubs.

Set amid scrub-covered hills, the open-pit mine yields up to 20,000 metric tons of cobalt annually, alongside significant copper volumes.

CMOC’s 2016 takeover of its controlling stake from U.S.-based Freeport-McMoRan marked a subtle but historic shift.

What once flowed west now courses east-into the hands of a party-state bent on irreversible entrenchment.

The Long March to Resource Security

China’s push to dominate rare earths and strategic metals began decades ago-with research institutes in the 1960s and state-led programs in the 1980s.

The strategy accelerated in the 2000s, when Beijing elevated resource security to a national priority.

At the time, China lacked sufficient reserves of many critical materials. But it had capital, policy, and patience.

While Western firms chased quick returns and fled “risky” regions, Beijing dispatched state enterprises.

Backed by the Go Out strategy and later Made in China 2025, Chinese officials struck deals in Indonesia for nickel, in Bolivia and Argentina for lithium, and across Africa for cobalt, copper, and rare earths.

They didn’t just buy mines-they built roads, railways, ports, and, most critically, refineries.

China now dominates cobalt and copper supply chains so entirely that few alternatives remain-and none match its scale or precision.

From Pit to Empire

In Katanga, minerals don’t wait to be dug before they’re claimed.

CMOC and consortia involving Sinohydro have secured majority stakes and long-term offtake agreements-locking in volumes before a single rock is moved.

Once processed into cobalt hydroxide or copper concentrate, the cargo moves-through Kasumbalesa at the DRC-Zambia border, then onto rail and truck fleets contracted to Chinese operators.

Whether routed via Dar es Salaam, Beira, or Lobito, the pattern repeats: infrastructure financed by Chinese loans, operated in alignment with Chinese interests, and scaled to serve Chinese supply chains.

At port terminals-many expanded with Chinese funding-cargo is loaded onto Chinese-chartered ships and steered through critical sea lanes like the Strait of Malacca. The destination is rarely in doubt: China’s coastal refineries.

Inside the country, firms like Huayou Cobalt, GEM Co., CNGR, and Jinchuan refine more than 75% of the world’s cobalt-and much of its copper-into battery-grade metal, powering everything from smartphones and EVs to drones and hypersonics.

China calls it supply-chain resilience.

Others see a mineral chokehold-modern in form, colonial in function.

Breaking Beijing’s Grip

But the grip is beginning to slip.

In Kinshasa, the DRC is auditing Chinese contracts, demanding $17 billion in overdue infrastructure, and warming to Western offers that don’t require sovereign concessions.

Gécamines-Congo’s state-owned miner-has grown more assertive, resisting deeper Chinese consolidation amid quiet U.S. and EU engagement.

The West, long absent, is scrambling to catch up.

The U.S.-backed Lobito Corridor offers a new export route to the Atlantic, bypassing Chinese-controlled chokepoints. Europe, Canada, and Australia are investing in refineries, terminals, and rail of their own.

Everyone wants an alternative-because a Chinese dollar buys not just the critical resource, but the right to decide who docks, where, and when.

That leverage rarely stays economic for long.

Doraleh Port in Djibouti began as commerce. Months later, it became China’s first overseas military base.

According to the Africa Center for Strategic Studies, at least ten African ports have hosted PLA Navy ships and personnel in recent years. The line between trade and projection-especially under authoritarian regimes-is always thin.

Meanwhile, China is exporting its DRC playbook to new frontiers-Brazil among them.

Baiyin Nonferrous acquired the Serrote copper mine for $420 million, marking its first major foothold in Latin American copper. Over a third of Brazil’s copper now flows to China-and the share keeps rising.

That’s the backdrop colliding with Trump’s forever trade war.

In Brasília, Washington’s latest copper tariff is falling flat. Lula rejected what he called “tutelage”-the notion that the U.S. can punish Brazil over Bolsonaro’s prosecution.

So, Latin America’s largest economy will lean more heavily on China in the interim.

Last month, Trump’s team also stumbled in London, failing to secure rare earths for U.S. defense stockpiles. Beijing withheld export licenses for key magnets like samarium. The few granted cover only civilian buyers-and expire in six months.

Treasury Secretary Scott Bessent denied any quid pro quo, insisting AI chip restrictions remain. But F-35 magnets and copper wiring are still out of reach. Without alternatives, Pentagon supply chains risk seizing up.

So what began as a story about cobalt and copper ends as a parable of spheres of control-etched into chokepoints of geography and industry, shaped by those who can shut them down when it counts.

Because beneath the hum of cranes and the tango of trade lies a system under siege-where shipping lanes double as pressure points, and every container of strategic minerals shipped could be the final twist in a critical materials chokehold.