![기축통화로서 미국 토토사이트 bts화의 패권을 연방준비제도가 시스템적으로 지키고 있는 가운데 기술 진보와 지정학적 요인으로 중국의 위안화, 스테이블코인 등이 통화 주도권을 놓고 경쟁하는 국면이 예고되고 있다. [게티이미지]](https://wimg.heraldcorp.com/news/cms/2025/06/17/news-p.v1.20250617.1278832edd81466195d7c01a0b0dae6b_P1.jpg)

글로벌 국내총생산(GDP)과 무역에서 미국 경제가 차지하는 비중은 줄어들고 있지만, 국제 통화 시스템에서 미국 토토사이트 bts의 역할은 확대되고 있다. 실제로 여러 지표에서, 그리고 국제금융위기 이후 토토사이트 bts의 지배력이 더욱 커져 글로벌 화폐 단위라는 토토사이트 bts의 근본적인 역할이 주목받고 있다. 토토사이트 bts의 중심성은 글로벌 GDP나 무역 내 미국 경제의 중요성을 반영한다기보다 국제 금융에서 토토사이트 bts의 역할에서 비롯된다.

이처럼 무역과 세계 경제에서 미국의 지배력이 예전 같지 않음에도 토토사이트 bts가 더욱 강세를 보이는 분명한 역설로부터 국제 통화 시스템이 더 이상 무역 기반이 아니라 금융화되었다는 중요한 측면이 드러난다. 토토사이트 bts의 지배력은 미국의 수입 또는 수출 규모에서 비롯되는 것이 아니다. 토토사이트 bts의 지배력은 미국 금융 시장의 깊이, 유동성, 규모, 글로벌 부채와 상품의 토토사이트 bts화 표시, 그리고 무엇보다도 미국 연방준비제도(Fed)의 국제 금융 안전판 역할에서 비롯된다.

사실상 국제 통화 시스템은 현대판 브레턴우즈 체제로 진화한 셈이다. 나는 이러한 현대판 브레턴우즈를 금융화된 브레턴우즈라고 부르고자 한다. 이처럼 고도로 금융화된 세계 경제 속에서 고정환율은 자본 이동성으로, 금은 새로운 안전 자산인 국채로 대체되고 있다. 그렇게 토토사이트 bts 체제의 도전 과제는 주로 토토사이트 bts의 국제 금융 역할 약화에서 비롯된다.

미 토토사이트 bts와 토토사이트 bts 증권은 사실상 세계 경제의 기반 통화다. 다음과 같은 몇 가지 주요 지표들을 통해 토토사이트 bts 지배력의 핵심 요소들을 파악할 수 있다.

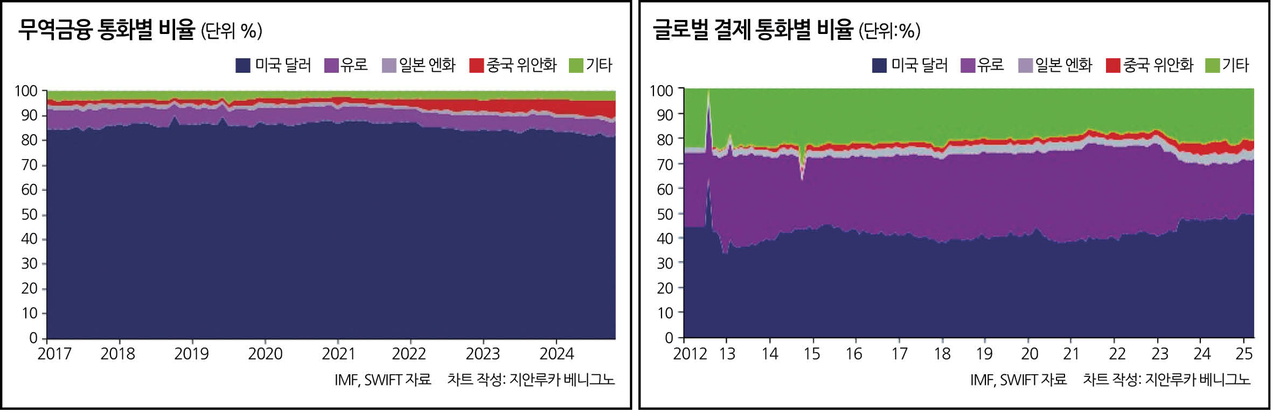

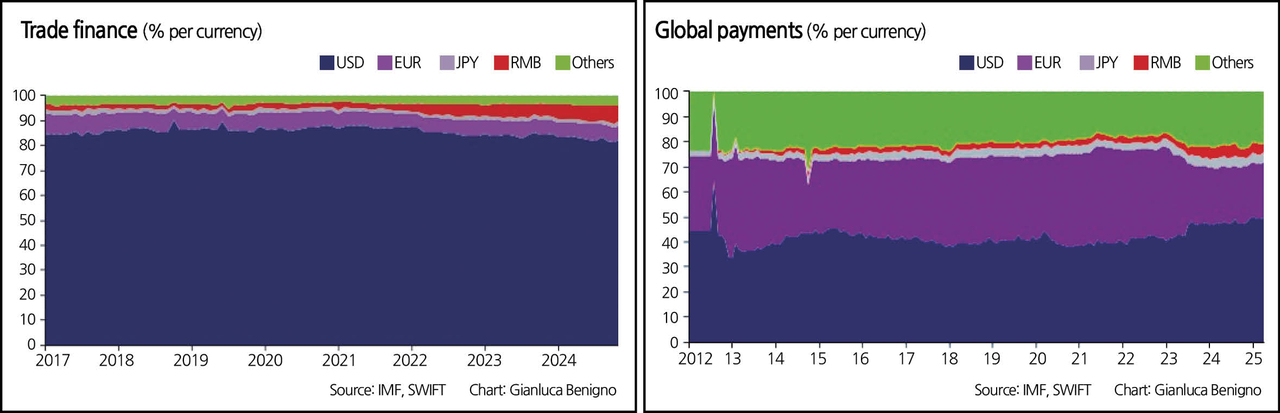

①중앙은행들은 외환을 보유할 때 여전히 토토사이트 bts를 주요 기축 통화로서 선호한다. 국제통화기금(IMF)의 데이터에 따르면 전 세계 외환보유고의 약 60%가 미 토토사이트 bts로 보유되고 있다.

②토토사이트 bts는 매개 통화 역할을 한다. 즉 국가들이 미국과 직접 거래하지 않더라도 무역 송장과 상품 송장이 토토사이트 bts로 표시된다는 뜻이다.

③토토사이트 bts는 국제 금융 인프라의 중심에 있다. 글로벌 무역 및 금융 거래의 결제와 청산이 이뤄지는 SWIFT 네트워크는(국제 거래가 토토사이트 bts로 표시됨에 따라) 미국의 환거래은행을 중심으로 운영되고, 따라서 미국의 법규를 따른다.

연방준비제도는 자체적으로 보유한 토토사이트 bts의 금융화 수단을 효과적으로 사용해 이런 구조를 강화해왔다. 실제로 위기 발생 시 스왑 라인과 FIMA 리포제도를 통해 긴급 유동성을 제공하는 곳은 IMF나 다른 다자간 기관이 아닌 연방준비제도다. 이러한 개입을 통해 토토사이트 bts 시스템은 글로벌 쇼크 기간에 더욱 매력적으로 변모하고 안정화되면서 효과적으로 완성됐다. 실질적으로 연방준비제도의 기구들은 금융화된 토토사이트 bts 시스템을 위한 지원을 제공한다.

이러한 국제 통화 시스템의 금융 기반은 최근 미국 정책(관세 및 제재)의 변화가 가지는 함의, 그리고 이 변화가 토토사이트 bts 시스템의 내구성과 어느 정도 상충하는지를 분석하는 데 핵심적인 역할을 한다.

토토사이트 bts의 금융 무기화와 새로운 지경학적 대립

오랫동안 토토사이트 bts의 글로벌 역할은 국제 금융의 닻을 제공하는 안정성의 원천으로 여겨져 왔지만, 최근의 사건들로 인해 이 체제의 이면이 드러났다. 토토사이트 bts는 중립적이고 안정적인 통화일 뿐만 아니라 경제의 지리적 대립에 사용될 수 있는 지정학적 도구이기도 하다는 점이다.

러시아의 우크라이나 침공 이후 토토사이트 bts는 명백히 무기화됐다. 대응책으로써 미국과 동맹국들이 러시아 중앙은행의 보유고를 압류하고 러시아 은행들을 SWIFT 결제 시스템으로부터 차단한 것이다.

이 사건으로 인해 토토사이트 bts 체제 참여에 대한 유인책 구조가 근본적으로 변화했고, 특히 토토사이트 bts화에서 벗어나 다변화하려는 신흥 시장과 전략적 경쟁국 간의 노력이 가속화했다.

현재 무역 분쟁에서 가장 중요한 것은 중국에 대한 입장이다. 초기에 발표된 파격적인 관세와 그중 부분적으로 철회된 관세는 궁극적으로 두 최대 경제국 간 전략적 디커플링 가능성을 명확히 보여준다. 이러한 디커플링은 중국 경제의 재편 또는 국제 통화 질서의 재구성으로 이어질 수 있으며, 각국은 토토사이트 bts에 덜 의존하는 유사 체제 또는 대체 금융 네트워크를 모색할 것이다.

마지막으로 미국의 경제력 확대 수단을 대표하는 최신 법안이 있는데, 바로 최근 하원에서 통과된 ‘불공정한 외국 조세에 대한 제재 집행(Enforcement of Remedies Against Unfair Foreign Taxes)’ 법안에 포함된 ‘섹션 899’ 조항이다. 이 조항은 미국 정부가 ‘차별적’이라고 간주하는 조세 정책을 시행하는 관할권 내 개인과 기업을 대상으로 한다. 이 투자자들이 벌어들이는 이자, 배당금 등 불로소득에 대한 세율을 인상할 것을 제안하고 있다. 만약 해당 조치가 확정되면 토토사이트 bts의 금융 무기화에 한 차원이 더 추가돼 미국 금융시장에 대한 접근성 및 토토사이트 bts 기반 중개의 혜택이 미국의 재정적 및 지정학적 우선순위에 따라 점점 더 조건부로 전환될 수 있음을 시사한다.

대안적 전개 상황

특히 중국은 토토사이트 bts에 대한 의존도를 낮추거나 위안화(RMB)의 사용을 촉진함으로써 이 상황에 대응해 왔다. 중국 정부가 취한 조치들은 ▷주요 전략적 교역국, 특히 러시아 및 이란과의 양자 간 위안화 무역 ▷위안화 결제 및 청산을 촉진하기 위해 SWIFT의 중국판 대안인 CIPS 개발 ▷중국인민은행의 위안화 사용 전략적 스왑 라인 개설 등이다.

그러나 이러한 노력에도 위안화는 전 세계 결제 및 외환보유고의 3%만을 대표한다는 점에서 토토사이트 bts의 경쟁 상대가 되지 못하고 있다.

국가 주도의 대안뿐만 아니라 기술의 발전 또한 민간 부문의 디지털 혁신을 통해 새로운 가능성을 제시하고 있다. 구체적으로 비트코인을 비롯한 암호화폐들은 탈중앙적인 대안을 제공하고 있으나, 가격 변동성과 제도적 지원 부족으로 인해 이들이 주류로 사용되는 데에는 한계가 있다.

스테이블코인 중에서도 USDT와 USDC처럼 토토사이트 bts에 고정된 것들이 국경 간 결제에서 가장 신뢰할 만한 대안으로 떠오르고 있다. 역설적으로 이들은 여전히 토토사이트 bts와 연동돼 있지만 전통적인 은행 시스템 밖에서 운영되는 토토사이트 bts의 대체재로 발전할 수 있다.

한편, 각국의 중앙은행은 CBDC(중앙은행 디지털 화폐)를 연구하고 있다. 이러한 노력이 전 세계적으로 조율된다면 궁극적으로 글로벌 결제에 대한 마찰 및 토토사이트 bts 의존도를 줄일 수 있을 것이다.

하지만 모든 대안의 근본적인 도전 과제는 기술적인 것이 아니라 제도적인 것이다. 통화 지배력은 법적 인프라, 재산권에 대한 신뢰, 깊고 유동적인 금융시장, 그리고 믿을 만한 정책 구조에 달려 있다. 토토사이트 bts는 이 모든 요건을 갖추고 있는 반면, 그 어떤 디지털 대안이나 위안화도 현재로서는 모든 요건을 충족하지는 않는다.

미래의 균형 상태로서의 토토사이트 bts 파편화?

여기서 생각해 볼 수 있는 최종 결과물은 토토사이트 bts 파편화 시나리오라고 주장하고 싶다. 토토사이트 bts 파편화 하에서는 어떤 단일 토토사이트 bts도 지배적이지 않다. 다음과 같은 배열이 구조화될 수 있다.

▶미국과 미국의 서방 동맹국, 라틴아메리카, 석유 수출국을 포함하는 토토사이트 bts 블록

▶아시아의 일부 지역, 러시아, 그리고 중국의 일대일로 파트너국을 포함하는 위안화 블록

▶은행 없이도 국경 간 결제를 가능케 하는 디지털 토토사이트 bts 또는 스테이블코인 통로

토토사이트 bts적 효율성이 떨어지는 이 복잡한 시스템은 거래 비용은 증가시키고 유동성은 감소시킬 수 있기 때문에 어떻게 작동할지 분명치 않다. 동시에 이는 단일 금융 패권국을 중심으로 하는 토토사이트 bts가 아닌 다극적 세계 토토사이트 bts를 반영하는 결과물이 될 수도 있다.

결론

현재 미국의 정책은 토토사이트 bts의 특권적 지위를 약화할 수 있다. 그러나 고도로 금융화된 현재 구조의 경제적 안정성은 대안 개발에 상대적으로 높은 비용을 부과한다.

그러나 현재로서는 토토사이트 bts의 규모와 제도적 깊이에 필적할 만한 경쟁자가 없다. 미국 토토사이트 bts가 여전히 지배적이지만, 그 우월적 지위가 점점 줄어들며 의문이 제기되고 있다. 기술 발전과 더불어 급진적인 정책 변화가 파편화된 통화 시스템의 활로를 열어줄 수 있다고 생각한다.

지안루카 베니그노는 누구

스위스 로잔대 경제학과 교수로 재직 중이다. 미국 캘리포니아대 버클리 캠퍼스에서 국제 거시경제학 박사 학위를 취득했다. 환율 경제학, 국제 토토사이트 bts 정책 협력, 거시건전성 정책 등의 분야에서 전문성을 인정받고 있다. 영란은행, 국제토토사이트 bts기금(IMF), 미주개발은행(IDB)에서 여러 컨설팅 역할을 맡았다. 미 뉴욕 연방준비은행에서 선임 이코노미스트로 활약(2007~2008년)했다. 런던정경대에서 종신교수로, 미 프린스턴대에서 방문교수로 각각 일했다.

![While the Federal Reserve is systematically safeguarding the hegemony of the U.S. dollar as the key global currency, technological advancements and geopolitical factors are signaling an emerging phase of competition for monetary dominance from China’s yuan and stablecoins. [Getty Images]](https://wimg.heraldcorp.com/news/cms/2025/06/17/news-p.v1.20250617.a25d717568194b5bbc1505d932475f69_P1.jpg)

The Challenges to Dollar’s Dominance

Although the share of the U.S. economy in terms of global GDP and in global trade has been declining, the role of the U.S. dollar in the international monetary system has expanded. In fact, by many measures, and even more so in the aftermath of the global financial crisis, the dominance of the dollar has increased, further stressing its fundamental role as the global monetary currency. The centrality of the dollar arises from its role in global finance as opposed to a reflection of the importance of the US economy in terms of world GDP or world trade.

This apparent paradox—that the dollar grew stronger even as the U.S. becomes relatively less dominant in trade and in the world economy—reveals a critical aspect: the international monetary system is no longer primarily trade-based, but is financialized. The dollar’s dominance does not arise from the volume of U.S. imports or exports. The dollar’s dominance arises from the depth, liquidity, and scale of U.S. financial markets, the denomination of global debt and commodities in dollars, and importantly, the role of the Federal Reserve as a global financial backstop.

Effectively, the international monetary system has evolved into a modern version of Bretton Woods. I would refer to this modern Bretton Woods as a financialized Bretton-Woods. In this highly financialized global economy, capital mobility has replaced fixed exchange rates, and Treasuries have replaced gold as safe assets. Challenges to the dollar system arise then mainly, from the undermining of its global financial role.

The USD and dollar securities are indeed the infrastructure currency of the world economy. The pillars of dollar dominance can be captured by some key metrics:

• Foreign reserve holdings by Central Banks still favor the dollar as the main reserve currency. According to data from the IMF, about 60% of global foreign exchange reserves are held in U.S. dollars.

• The Dollar serves as a vehicle currency (Goldberg and Tille, 2008): this means that trade invoices and commodity invoices are denominated in dollars, even if countries are not directly trading with the US

• The Dollar is at the center of the Global Financial Infrastructure: the SWIFT network, through which global trade and financial transactions are settled and cleared, is centered around U.S. correspondent banks (since global transactions are denominated in dollars) and, as such, is subject to U.S. regulations and law.

This structure has been strengthened by Federal Reserve tools that effectively have ringfenced this financialized version of the dollar system. It is indeed the Federal Reserve (not the IMF or other multilateral institutions) that, when a crisis occurs, provides emergency liquidity via swap lines and the FIMA repo facility. These interventions have effectively completed the dollar system, reinforcing its appeal and stabilizing it during global shocks. In effect, the Federal Reserve facilities offer the support for the financialized dollar system.

This financial foundation of the international monetary system is key for analyzing the implications of recent shifts in U.S policy (tariffs and sanctions) and the extent to which these shifts challenge the durability of the dollar system.

The Financial Weaponization of the Dollar and the Emerging Geoeconomic Confrontation

While the global role of the dollar has long been seen as a source of stability, as it provides an international financial anchor, recent events have exposed the other side of this system: the dollar is not just a neutral stable currency but is also a geopolitical instrument that could be used in geo-economic confrontation.

The weaponization of the dollar became evident following the Russian invasion of Ukraine. In response, the United States and its allies seized Russia’s central bank reserves and cut Russian banks off from the SWIFT payment system.

This particular event fundamentally changed the incentive structure behind participation in the dollar system and accelerated efforts, particularly among emerging markets and strategic competitors, to diversify away from the dollar.

In current trade disputes what matters the most is the stance vis-à-vis China: the steep tariffs announced early and partially reversed give a clear indication of the eventual possible strategic decoupling between the two largest economies. This decoupling could result in a) a redimensioning of the China economy or b) a restructuring of the global monetary order, with countries seeking parallel systems or alternative financial networks less dependent from the dollar.

Finally, a latest measure representative of the expanding toolkit of U.S. economic power is Section 899, a provision included in recent legislation passed by the House and titled “Enforcement of Remedies Against Unfair Foreign Taxes.” This provision targets individuals and companies from jurisdictions whose tax policies are deemed “discriminatory” by the U.S. government. It proposes raising tax rates on passive income, such as interest and dividends, earned by these investors. This move, if confirmed, adds another layer to the financial weaponization of the dollar, signaling that access to U.S. financial markets and the benefits of dollar-based intermediation may become increasingly conditional on alignment with U.S. fiscal and geopolitical priorities.

Alternative Developments

China, in particular, has responded by seeking to reduce its dependence on the dollar or to promote the use of the RMB. There are several measures undertaken by the Chinese leadership:

• Bilateral trade in renminbi (RMB), especially with Russia, Iran, and other key strategic partners.

• The development of CIPS, a Chinese alternative to SWIFT, to promote clearing and settlement in RMB.

• The creation of strategic swap lines by the People‘s Bank of China in RMB.

However, despite these efforts, the RMB is still a distant competitor to the dollar, accounting for less than 3% of global payments and foreign reserves.

Beyond state-driven alternatives, technological development is adding new possibilities through private sector digital innovation. Specifically, Bitcoin and other cryptocurrencies offer decentralised alternatives, but their price volatility and lack of institutional backing limit their mainstream usage.

Stablecoins, particularly those pegged to the dollar (like USDT and USDC), have emerged as a more credible alternative for cross-border payments. Ironically, these are still tied to the dollar but might evolve into dollar substitutes that operate outside the traditional banking system.

Meanwhile, central banks are exploring CBDCs (Central Bank Digital Currencies). One possible benefit of these efforts, if coordinated internationally, is to eventually reduce the friction and dollar-dependency of global payments.

Still, the fundamental challenge for any alternative is not technological but institutional. Currency dominance relies on legal infrastructure, trust in property rights, deep and liquid financial markets, and credible policy frameworks. The dollar still enjoys all of these, while neither digital alternatives nor the RMB currently meets all the requirements.

Monetary Fragmentation as a Future Equilibrium?

Here, I argue that a possible eventual outcome is a scenario of monetary fragmentation: under monetary fragmentation, no single currency dominates. A possible configuration could be structured around:

•A dollar bloc, including the U.S., its Western allies, Latin America, and oil-exporting countries.

•A RMB bloc, encompassing parts of Asia, Russia, and China’s Belt and Road partners.

•A digital currency or stablecoin corridor enabling cross-border settlements without banks.

It is not obvious how such a complex system would work, as it might be less economically efficient, potentially increasing transaction costs and reducing liquidity. At the same time, it might be a reflection of a multipolar world economy as opposed to one centered on a single financial hegemon.

Conclusions

Current U.S. policy might undermine the dollar’s privileged position. The economic stability of the current structure, centered around a highly financialized structure, though, imposes relatively high costs in developing alternatives.

Yet, for now, no credible competitor matches the dollar’s scale and institutional depth. The USD remains dominant, but its margin of supremacy is shrinking and is questioned. I suggest that drastic policy shifts, along with technological developments, might pave the way towards a fragmented monetary system.